SpaceX went public last week, and while I’m not adding to the valuation noise (though I could), I want to orient towards a more impressive feat than a $2T IPO. For better or worse, the public stock market just gave a record ovation to a company that it could never have built.

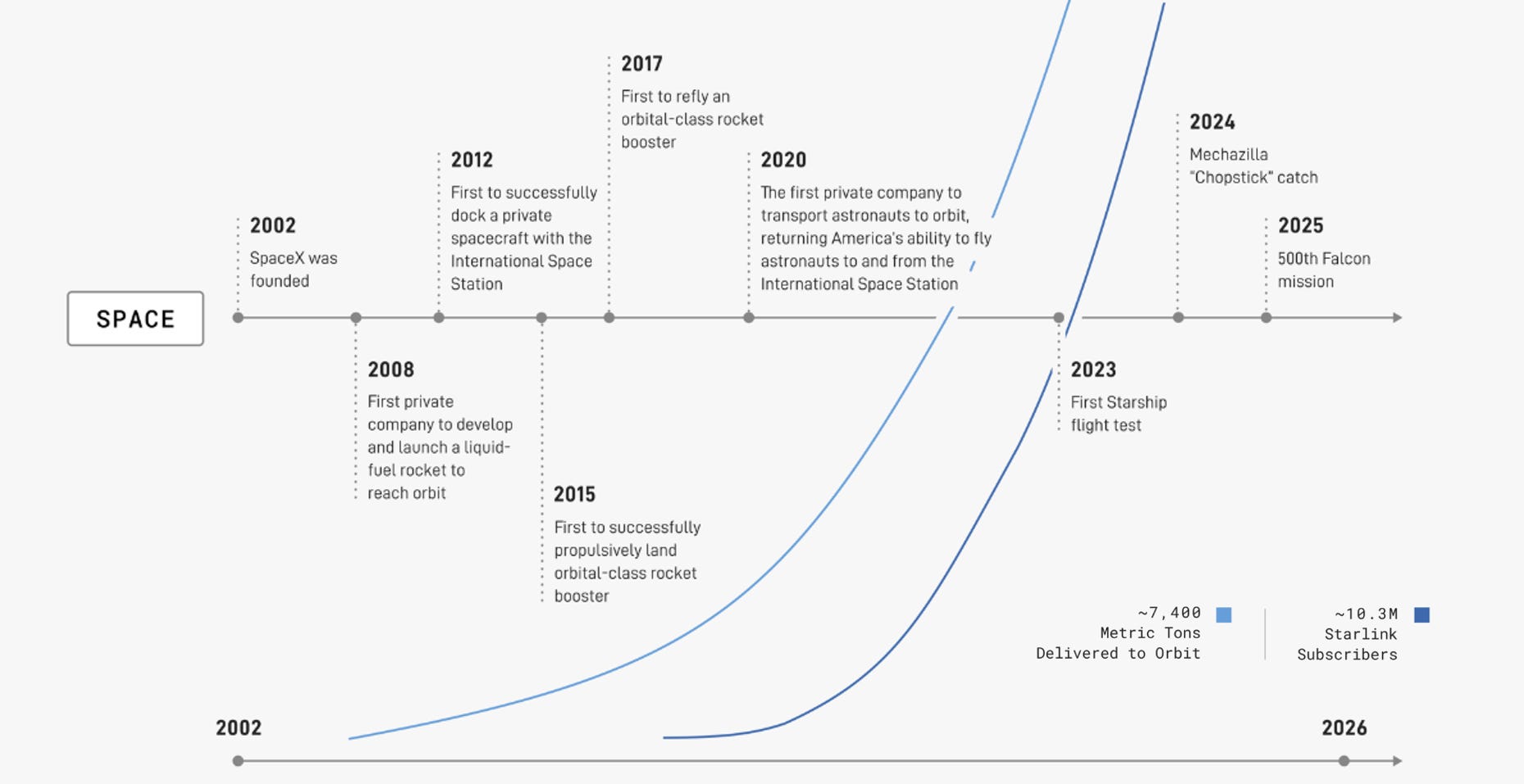

Musk started SpaceX in 2002, back when the American launch industry was a dying business. It burned cash for years on something serious people called delusional, and it didn’t turn cash-flow positive until around 2015. Even now the only part that reliably makes money is Starlink. No public-market investor would have touched that timeline: twenty years to profitability, billions sunk along the way, the promise unproven and the market not existing for most of the route. And yet here we are, begrudgingly clapping at the receipt.

That receipt took twenty years to print. While I’m no particular fan of Mr. Musk, I do find it admirable that he made a decision to invest in duration.

A talent we traded away

Investing in duration means putting capital and work behind something whose payoff is years out, far from certain, and staying in through the hard middle. The middle is long, there’s nothing to show for it, and every instinct, critic, and friend you have is telling you to quit.

We used to be good at this. The railroads, the interstates, Apollo program, Bell Labs, the whole postwar industrial build — none of it would survive a modern earnings call, but the people of the past did all of it anyway. Somewhere we traded that muscle for creation for a less patient one.

You can roughly point to when it started: the Jack Welch era. That’s when the smooth, always-rising earnings line became the actual product a company made, and the business itself became the thing you squeezed to produce it. You managed the stock and the company itself barely mattered. And you can see the toolkit everywhere after that. Buy back the stock instead of building a plant. Sell off key assets for a buck. Bring in the activist investor whose whole job is to make sure you stop spending money on anything that won’t pay off before he sells. And Managers with exclusively short-term incentives.

The other side has a point: short horizons keep people honest. Money should go where it’s most useful right now, not sit forever inside some CEO’s twenty-year vanity project, and plenty of so-called patient investment is just empire-building dressed up as vision. Fine. But we didn’t stop at honest. We made ninety days the only length of time anyone’s allowed to think in. A market that can only see ninety days out has no way to register anything that takes longer than a fiscal year to build, and nobody decided that on purpose; it’s just how the wiring works now.

We’d rather close the mill than improve it

Once you notice it, the ninety-day mind is everywhere, and it usually shows up the same way. Squeezing more out of what already exists than building the thing that lowers costs, improves quality, or otherwise doesn’t yet exist. An extractive economy, to reference my previous work.

The version that frustrates me the most is when we opt for profitability over production. We sooner close a working mill to protect monopoly pricing power before we invest the capital to make that mill competitive to run and allow for induced demand to show its face. Protecting margin is something you can do this quarter and put in the deck. Lowering a cost curve may take ten years and pay off long after whoever approved it has moved on. So, we protect the margin, and then we call it discipline, when really it was just the version of the decision that we could put a number on.

That one instinct explains more than it should. Companies buy back their own stock instead of building anything (In a market where capital is plentiful, mind you). Our political culture chases whatever makes voters happy this cycle and ignores whether the country is still competitive in twenty years — and before anyone reaches for a team to blame, this isn’t a party problem, it’s an incentive problem; short-term comfort wins every election no matter who’s holding the power. Most of the hard things we’re stuck on, we already have the money and the know-how to fix. What we lack is the patience to spend now and collect later, even if it comes long after we’re gone, which is why they stay problems.

Another American mill, closed for business.

American automakers did exactly this to themselves over the last six months, in public.

America has had every advantage, nearly 100 years of Auto dominance. The engineers, the factories, well over a decade of warning this was coming, and enough cash to fund the switch twice over and a rising signal in the form of Tesla’s rise in the early 2010s. However, unfortunately for American investors, building a real EV business is the kind of inconvenience bet that only pays off after years of losing money first: new batteries, new software, supply chains that don’t yet exist, all of it paid for long before the business earns a cent. It was a duration problem, and automakers blinked.

Actually, “blinked” is too kind. They gave up. In a few months Ford, GM, and Stellantis wrote down something like fifty-five billion dollars ($55,000,000,000, or the annual consumption of a small city) on their EV programs, and Ford’s piece alone was the biggest EV write-down in the history of the American car business. They killed the F-150 Lightning, the electric version of their most important vehicle. At the Detroit Auto Show this January the EVs were a softly avoided story, and everyone was back to talking up hybrids and updated gas trucks. They ran back to the trucks that make money this quarter and walked away from the future, because the future was going to cost them ten years of actual investment, actual capital deployment, actual innovation. The good news is: American investors, while fighting to deploy capital into the secondary markets, received nearly $100B in buybacks and distributions from these companies over the past 20 years, lucky us.

That’s the mill, exactly. They pulled out the cash until the mill couldn’t compete and are giving up on improving that mill until it rusts to a halt, all while closing our markets to real competition to protect our sleeping giants from having to make real investments, just because future demands real innovation, real risk, and short-term negative free cash flow.

Now look at who took the other side of that bet, the same ones whose products are banned from competing. China spent more than fifteen years on it, they were patient, and they were ruthless about it. They subsidized the batteries and built out the supply chain. They sat through years of losses and a savage fight among their own companies, and they let a battery maker like BYD slowly turn into one of the best car companies in the world. Chinese auto brands have gone from under three percent of the global market to about eleven, and they’re building plants in Europe now that make western import tariffs close to pointless. Ford’s own CEO has compared this to the arrival of the Model T, and he’s said the competition he’s scared of isn’t the other old carmakers. It’s the Chinese.

Even though their market is in a disarray of creative destruction, we should be worried that the survivors didn’t dodge the pain of the long game. They went straight through the middle of it. Meanwhile, we just walked off the field and took a vacation, paid for by depreciating balance sheets.

The most expensive thing we won’t build

Housing is the one that keeps me up at night. Same disease, working on the problem I care about more than any other, particularly here in California.

It’s a long-horizon problem from every angle. Getting real supply built takes ten or fifteen years once you count the planning and the permitting and the financing and the building itself. And every incentive in the system runs the other way. If you already own a home, more supply is a threat to your biggest asset, so you fight it. If you’re a local official, you get rewarded for killing the unpopular project this year, and nobody ever blames you for the homes that don’t get built a decade out. Nobody anywhere in that chain gets rewarded for the houses that quietly exist in fifteen years.

So, we end up with a disaster slow enough that everyone can watch it happen while nobody does much about it. Not for lack of land or money or workers or knowledge or interest; we have all of that. We just won’t wait. We won’t take the discomfort. It is the clearest case I know of what short-term thinking does to a place: it can take the most important problem you’ve got and make it unsolvable in practice, even while everyone in the picture is behaving rationally in their own ninety-day outlook.

And housing’s just the most obvious version. The same thing quietly guts whole regions — the smaller towns and overlooked markets where somebody patient could build something that lasts, if they were willing to wait around long enough to find out.

Where I try to practice it

I could leave this as an argument about money and markets, but that’s not really how I think about it. For me the long game is as much about business and investing as it is about people.

I bet on people, like I mentioned in my last post: the fastest compounding, untaxable investment I have is my network. Most of the relationships I put real time into will never pay off in a way I could point to on a spreadsheet, and that is fine, because the whole premise is that if you keep showing up for people without keeping score, a decade later the trust you built is the thing quietly routing work and ideas and the occasional out-of-nowhere introduction back in your direction. I’m not trying to get something out of the person in front of me. I’m trying to build a little trust and then leave it alone. It never comes back on a schedule you’d have chosen.

It’s the same bet as the rocket and the cheaper battery, shrunk down to one conversation at a time. You spend now, you get nothing visible back, and the whole thing only makes sense if you plan to still be around in ten years. The move never changes. The only thing that changes is what you’re counting it in.

The few who think in decades

The thing I’d want you to take from all of this: the long game isn’t about being noble. It’s an actual edge, and the reason is embarrassingly simple. Hardly anyone will stay in something long enough to get the payoff, so the patient opportunities just sit there underpriced. Nobody is bidding against you on the stuff that takes ten years.

Which is why I’ve mostly stopped complaining about it. I started using it as a filter instead, a way to find the people I want around me. There’s a small group out there who just don’t run on the ninety-day clock, and they’re easy to miss because they keep quiet about it. You’ve probably met one or two: the founder building for fifteen years with no interest in flipping, the operator who’d fix the mill before stripping it for parts, the person who can drive through a town everyone wrote off and see something there. They don’t make much noise, but they’ll be still standing there, looking like an overnight success, ten years on while the people chasing quarters have already moved to the next thing, and the thing after that.

That’s the group I’m trying to build, and it’s more and more where my own work is heading: economic development aligned investing in the places everyone else skipped, putting patient money into overlooked people and communities with patience for real compounding to take place. The work is entrepreneurship, real industry, maybe housing, and the slow unglamorous build that never photographs well.

If you already think on a longer clock, or you want to and you’re sick of pretending ninety days counts as a plan, then reach out (Duncan@saorsapartners.com). Tell me what you’re building and how far out you’re really looking, and you’ll receive an invite to our Slack - filled with long-duration Operators and Investors. Those are the relationships we care about most: no quick payoff, and ten years of upside.

The receipt takes years to show up. But the decision behind it doesn’t take long at all. You just have to be willing to look stupid for a while, longer than is comfortable, while everyone optimizing for the quarter moves on to the next thing and the one after that. That’s most of the trick. The rest is finding the few people willing to wait it out with you.