Every year I lose Christmas. I’m not a great gift giver, and I’m an even worse gift recipient, but this year I won it. realizing the years are flying by, I gave everyone in my family an experience: visits to historical railways, urban jungles, a K-pop festival, and for my sisters, a weekend in Napa.

We took that trip last week, ahead of a conference I had down the road. Somewhere between a buttery Chardonnay and a turnaround consultant’s third glass, I worked out what I actually think about the SpaceX IPO.

Surrounded by an artisanal commodity, I realized that the margins running up and down the AI stack, models, compute, data centers, power, and applications, are going to compress, and compress hard, the moment the capital markets start to demand real returns from the consumer side of the market. Not a collapse, more likely an unwind that looks more like inflation than implosion: higher revenues, thinner margins, venture-grade businesses repricing into project finance. The technology is real. The capital structure stacked on top of it is not.

A Lifetime in a Barrel

White Rock Vineyard is a survivor of the 1970s Napa boom — founded in 1977, in the wake of the Judgment of Paris, and still run by the second generation. A decade later, they carved a cellar into the hillside to age their wine. Touring it, I had a flat, unromantic realization: every barrel is an accumulation of hours. Planted, trimmed, picked, crushed, fermented; years of labor sitting on the inventory side of the balance sheet, valued at the cost of the blood, sweat, and tears that went into it. As the wine ages it accumulates nothing but perceived value, while burning off 2% a year as the angel’s share.

That’s the first lesson: wineries are working-capital gluttons. One port producer I met carries as much as ten years of production cost as inventory. Which begs the obvious question, how on earth do you finance that?

Banking on Wine

At the conference later that week I had dinner with a community banker who has spent decades lending to Wine Country. Her answer: industry-specific lines of credit, capitalizing up to 50% of the wholesale price of every gallon of Napa Valley wine. A winery can seriously extend its ability to hold inventory on the bank’s dime.

I couldn’t help but chuckle, realizing my deposits are sitting in someone’s wine cellar, waiting to be enjoyed by a few ex-pizzeria gal pals celebrating their 50th.

“You’re thinking of this place all wrong, as if I had the money back in a safe. The money’s not here. Your money’s in Joe’s cellar, that’s right next to yours, and in the Kennedy cellar, and in Ms. Macklin’s, and a hundred others. You’re lending them the money to make wine, and they’ll pay it back the best they can.” — Napa’s George Bailey, It’s a Full-Bodied Life

Here’s the part to carry out of the cellar: The asset on the balance sheet is also the collateral against the loan that financed it. The price of the wine sets how much you can borrow; the borrowing sets how much wine gets made; the wine that gets made sets the price. The asset price is the borrowing base.

Fermented in a Different Market

The wine industry, as you may have heard, is going through “just a bit of a gully.” Long lead times from planting to fermentation to aging force a winery to forecast demand years out, and that forecast is inherently speculative: the same linear extrapolation that tripped up KTM coming out of Covid has guided most of Napa’s planting decisions, shared one winery turnaround consultant. Layer on seltzers and everything else displacing wine on the shelf, and you get the inventory glut now forcing non-harvests across the Valley.

One Wells Fargo wine banker shared that accumulated inventory has to move, and pushing supply into weakening demand drives the wholesale price down. From there the mechanics turn reflexive. Collateral-coverage requirements force still more product onto the market, prices fall further, lenders’ collateral positions deteriorate, and shrinking balance-sheet capacity pulls capital out of the system. Less credit means less leverage for land, which pulls the bank’s bid out from under asset prices.

And those prices were inflated to begin with, positive forward expectations roughly doubled vineyard farmland over the past decade. That capital arrived as one of two buyers. The fundamental buyer underwrites the vineyard on the cash it throws off. The speculative buyer is everyone else: the trophy purchaser, the family treating the estate as a store of value, the punter betting one of the first two shows up later at a higher price. As the industry strains, cash flows weaken and the fundamental bid recedes; downward pressure that causes the speculators to get spooked and leave. Each exit is a step-function cut to demand for a fixed-supply asset. What makes this case distinct is that the asset price is the borrowing base — inflated values justified more credit, and more capital inflated values. A bubble built on its own collateral, capable of unwinding at remarkable speed.

Now strip away the cellar romance, while a sommelier tastes a decade of decisions in the glass; everyone else tastes wine. For the connoisseur there is excellence. For the rest of the market, the part that actually clears the inventory, it’s just a fermented commodity fighting for market share against every other Friday buzz.

And commodities cycle. It’s the one thing they reliably do: a high price calls in capacity, the glut arrives, the price grinds down to the marginal cost of production, and as it turns out the only cure for low prices is, in fact, low prices. Even though the luxury tier floats above the weather; the commodity tier eats it.

Which is the real bridge to this capital landscape, because AI is commoditizing layer by layer. The models are converging. Compute is fungible by design. Inference is becoming a spot good you arbitrage across providers by the token. Strip away that romance — the AGI vintage notes, the founder’s artisan hand — and most of the stack is a commodity wearing venture multiples. And commodities don’t earn margins through the cycle. They earn the cost of capital.

So, What Does This Have to Do with Rockets?

The SpaceX IPO is astonishing, and I’ll keep my refined palate of unkind adjectives to one: speculative.

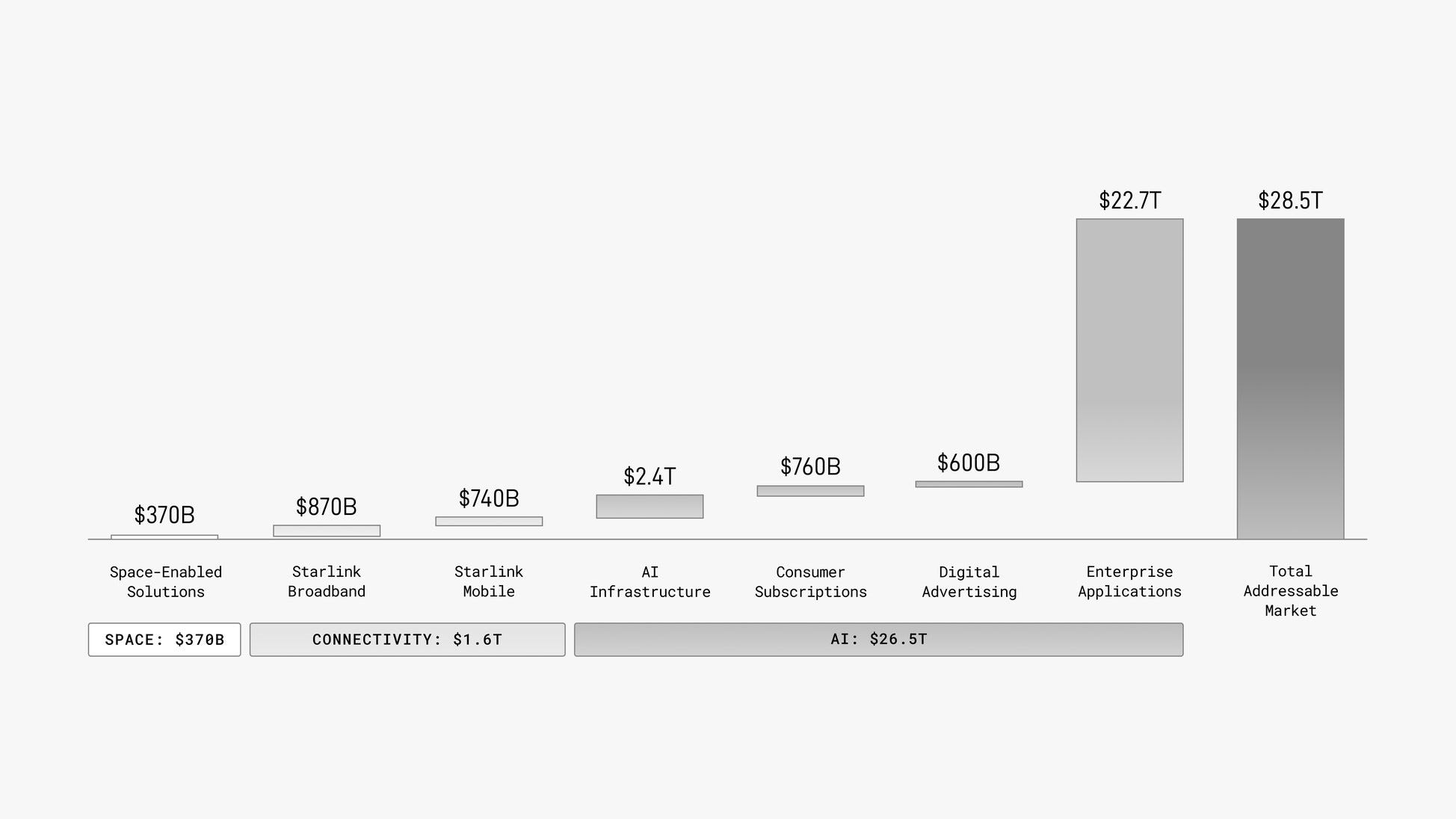

For the uninitiated, SpaceX is set to list north of a $1.75 trillion valuation and raise roughly $75 billion, the largest IPO in history. You’d think you were buying a space company. The one segment that reliably throws off cash is Starlink; the launch business reinvests everything it earns. What you’re actually buying, according to their market sizing expectations, aspires to be an AI company — Musk folded xAI (which had already swallowed X/Twitter) into SpaceX earlier this year, and the consolidated losses now flow almost entirely from that AI segment.

SpaceX’s Estimated TAM by Segment from SpaceX S-1 Filing pg. 172.

In the cellar the commodity and the collateral are two different objects: the wine is what cycles, the land is what the loan is written against. The land is scarce, and its scarcity is the floor — when the glut grinds wine down to marginal cost, the asset underneath still holds, and the spiral finds a bottom, even if the wine is sold at a loss. Compute is the opposite on both counts. A data center of GPUs isn’t scarce; it’s reproducible, and they are racing to build more of it. It doesn’t appreciate; it depreciates into obsolescence faster than wine ever evaporates. The thing that played the role of the floor is just another commodity, and a depreciating one at that.

So the same reflexive loop runs, with the floor knocked out. As an equity bet, the ‘collateral’ here isn’t really the hardware; it’s the profit in the chain, and that profit is circular: manufactured by the very inflows it is supposed to justify. Wine pledges a scarce asset while AI pledges its own circularity. One soft quarter on the subsidy side and the loop runs backward: thinner inflows, thinner profit, thinner justification for the inflows. The commodity cycle, with venture investors.

The bundle. SpaceX is the perfect specimen precisely because it looks like the wrong one. It is the least commodity-like company in the entire AI trade — Starlink and launch cadence are about as close to a scarce vineyard as anything in technology. Afterall, while the competitors were shouting “We build datacenters”, Mr. Musk had a stroke of creative genius stapling on “In-Space” to the end of it. Suddenly it's not a server farm, it's a vintage: notes of charred rocket, a metallic finish, and the soft rain that fell days before liftoff. This IPO takes a genuinely scarce asset, and pushes a capex burning commodity-compute core, while pricing the whole bundle on the vineyard story. The vineyard is real, but they’ve piled bagged wine in the cellar.

The margins. All of this justified as the commodity story itself sits on a supply chain whose margins may be a mirage. ASML and Lam at 30%-plus net, TSMC north of 40%, Nvidia nearly 65%, and the hyperscalers somewhere in the 15–35% band; while underneath all of it, demand for models sold to end users at a fraction of the loaded cost to produce, subsidized heavily by the capital inflows received by OpenAI, Anthropic, Google, Meta, and SpaceX. When capital floods a chain like this, the flood shows up as profit at every link. So, the question that should keep an allocator up at night: are these margins a real, or are they just your investment being captured down the chain? Consumption dressed as investment?

Because the end-usage is the whole question, and AI is a substitute good. It competes for the same task execution that human labor performs, which means its demand is ultimately bounded — and priced — against the marginal cost of the labor it replaces (which will reprice in response to its replacement). That’s an enormous ceiling. Global labor is the largest market there is. But it’s a ceiling set by economics, not by narrative, and the moment you wave the substitute away you’re back to the vintner planting on a straight line, right up until his P&L forces the realization that people are drinking White Claws.

How It Unwinds

So what cracks it? Not the technology, the financing. I’m not anti-AI; I’m against the speculative capital structure stacked on top of it. Watch the canary: the first undersubscribed round on the subsidy side. When the subsidy thins, compute has to fight the economics of the labor it replaces on honest terms, and the stack starts grinding toward marginal cost the way wine does.

It rolls downhill, layer by layer. Thinner subsidy means weaker projected demand for compute; weaker demand competes the margin out of the data centers; thinner data-center margins pull the bid out from under the chips; and a softer bid for chips reaches all the way back to the fabs, where the underwriting was written on straight-line growth and fat margins that no longer clear. This competition flips the incentive from scale to efficiency, which strands the least efficient chips (current generation), because they cost too much to run. Each layer reprices from a venture multiple to a project-finance one. Utilities, not unicorns.

The obvious objection is Jevons: make compute cheaper and you simply use more of it, keeping power draw and capex high. I think that’s right, and it’s exactly why I expect inflation rather than collapse. Cheaper, more efficient compute doesn’t kill demand; it lets AI percolate into the processes when it’s actually economic. Volume keeps climbing while margin per unit caves in. That’s the whole shape of the thing: the technology wins, the pool of activity grows, and the people who paid venture prices for utility cash flows are left holding the angel’s share, the value that evaporated from the barrel everyone assumed could only appreciate.