Back to Insights

($HIMS) Hims & Hers: The Pharma Brand Millennials and Gen Z Are Growing Up With

Duncan Young

Read on Substack

Saorsa Brief

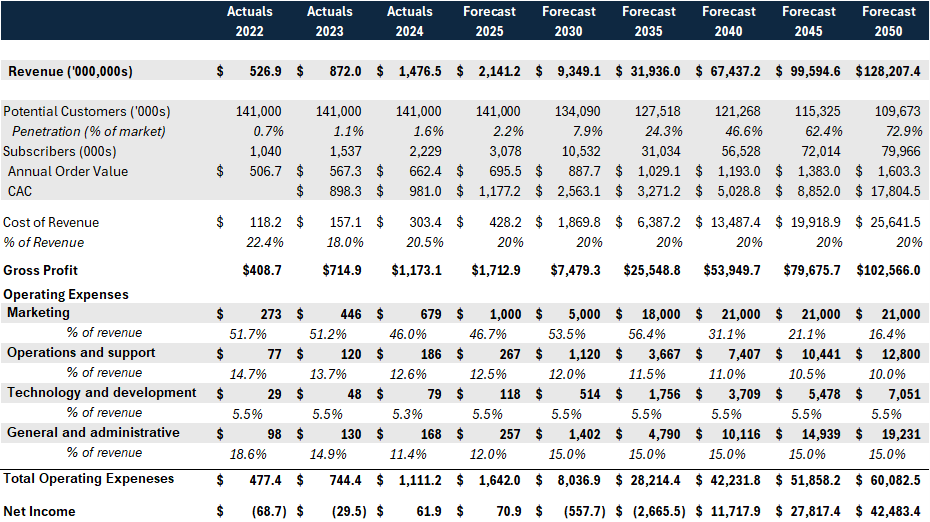

Saorsa Growth Partners brief on money and finance: Fundamental Financial Model Shows a 15% CAGR for 25 years. For founders and finance leaders pressure-testing growth and capital allocation. Designed as a 1-minute read.

At a glance

- Read time

- 1 min

- Published

- May 26, 2025

- Topics

- MoneyFinanceInvestment

Loading subscribe form…